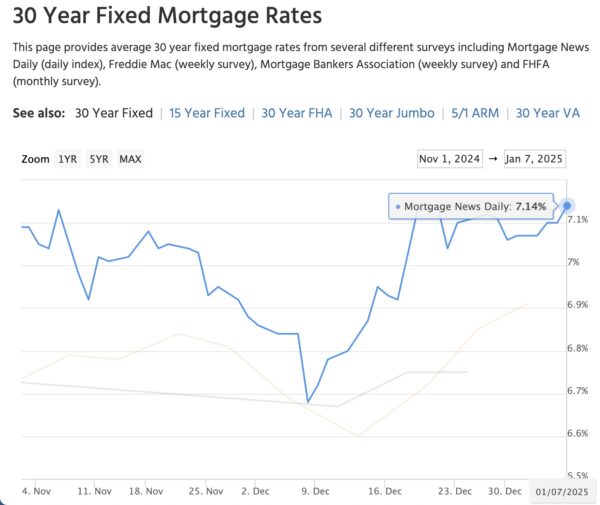

The Mortgage News Daily bumped up to 7.14% today, an increase from the frustratingly stable 7.10-ish levels we’ve been seeing since November. I am pretty sure all those pundits predicting mortgage rates in the 5’s were using Magic Eight Balls and wishful thinking. In their defense, those are probably some of the better techniques because predicting mortgage interest rates is pretty much impossible.

Mortgage rates are affected by just about anything in the economic universe, including the emotional state of investors. When they get nervous, they move their money around to make themselves feel better. Self-care is important! Those moves impact rates either up or down.

Take today’s news, for example. Two big reports came out: the Job Openings report, and the ISM Services PMI (!???) report.

The Job Openings and Labor Turnover Survey (JOLTS, cute, right!) released today for November shows all the signs of labor market stability. Sounds pretty good, right? Job openings have risen for two straight months, the first such streak since March 2022. We are now back above the 8 million threshold for the first time since May 2024. But, more job openings can lead to a higher cost of labor which is inflationary.

The ISM (Institute for Supply Management) Services PMI (Purchasing Managers’ Index) is a key indicator of the economic health of the service sector. This index includes industries like finance, healthcare, and retail. When this index rises, it suggests that the services sector is growing, with increased business activity and demand. The ISM Services PMI report for December showed that the PMI increased from 52.1 in November to 54.1 in December, compared to analyst consensus of 53.3. Numbers above 50 show expansion. Expansion? Everyone likes to see economic expansion except for someone looking for lower interest rates.

Investors took a look at this news – potentially higher labor costs and cost for services – and decided it a little too inflationary. They decided it was time to move some dinero out of the bond market so they could feel better. Money moving out of the bond market means higher mortgage rates for the rest of us. Breaking this down further:

Investor Behavior: Mortgage rates are also influenced by the bond market, particularly long-term bonds like the 10-year Treasury note. When the economy is strong, investors might expect the Fed to raise rates. That makes existing bonds, purchased at a lower rate, less attractive. As bond prices drop, their yields (interest rates) rise, and mortgage rates typically follow suit.

Economic Growth Signals: A rising ISM Services PMI indicates that businesses in the service sector are expanding, which is a sign of a growing economy. When the economy grows, people generally have more income, spend more, and invest more, which can increase inflation.

Inflation Concerns: As economic activity picks up, the risk of inflation (general rise in prices) grows. Lenders who offer mortgages are concerned about inflation because it reduces the future value of money. If lenders expect higher inflation, they may raise mortgage rates to compensate for this expected decrease in purchasing power.

Federal Reserve Actions: The Federal Reserve (the central bank of the U.S.) monitors economic indicators, including the ISM Services PMI, to decide on its monetary policy. If the ISM Services PMI suggests strong economic growth and potential inflation, the Fed may raise interest rates to cool down the economy. Higher interest rates from the Fed often lead to higher mortgage rates.

Incoming Adminstation: Looking forward, there is a lot of uncertainty about the economic policies of the incoming administration and that will impact the US economy, particularly in terms of inflation. All indicators point to a strong US economy, hence the Fed’s obsessive battle against inflation. Any policies that juice the economy further are going to exacerbate inflation and lead to higher interest rates. Investors may be hedging their bets right now.

Bottom line, we’ve got a strong US economy with signs of expansion. Despite the best intentions of Magic Eight Balls and wishful thinking, lower mortgage rates are not likely for some time.